Tax Return On-line : Guide to completing your UK tax return on-line and by post.

If you are self-employed, you are most likely required to complete a self-assessment tax return online. If you submit your tax return by post, you will need to complete, to arrive by 31st October. If you submit online, you will need to complete on 31st January the following year.

When do you need to complete your tax return?

As most tax payers know, tax is all about deadlines, missing a deadline is going to cost you money, and the longer you leave things, the more penalties you will receive. Get to know these deadlines, they are important!

If you have not already registered with Her Majesties Customs and Excise (HMRC), when you start your self-employment, become a sole trader, start a partnership, you need to register by the 5th October.

Once you are registered, there is a routine to your tax returns; we will use the tax year April 6th 2018 to April 5th 2019 in this example. Whatever year it is, the tax year always ends on the 5th April, and the new tax year always starts on the 6th April.

If you would like to send your tax returns by post/mail, you will need to make sure the forms arrive with HMRC by the 31st October following the end of year. Using our example tax year, the deadline for a paper return is 31st October 2019.

If you complete your tax return online, or use an accountant who submits returns online, you need to make sure this is done by 31st January. Again, using our example tax year, the deadline for an online return would be 31st January 2020.

If you would like HMRC to take payments from your PAYE wages to pay your self-assessment tax, you need to submit online before the 30th December, in our example, 30th December 2019.

It is possible HMRC will write to you with a different dead, this of course has precedence over any information here, or indeed elsewhere online.

When do you pay your tax bill?

However you submit your tax, whether it is a tax return online or by post, you need to settle your tax account (pay tax due) by 31st January. Using the example tax year above, payment in full must be made by 31st January 2020.

What are penalties for missing the deadlines?

If you are due to send a tax return, but have filed late, or not registered for self-assessment, you can be charged a penalty. If your tax return submission is up to three months late, you will receive a penalty of £100.00, even if you have no tax to pay!

After the initial three months, you will be charged £10.00 per day up to a maximum of £900.00.

After six months, you will receive a further £300 penalty or 5% of the tax due, whichever is the greater.

After a year, you will receive another £300 penalty or 5% of the tax due, whichever is the greater.

In addition to the late filing penalty, if you are liable to pay tax, you may also be charged a penalty for late payment, plus interest on the total amount owed.

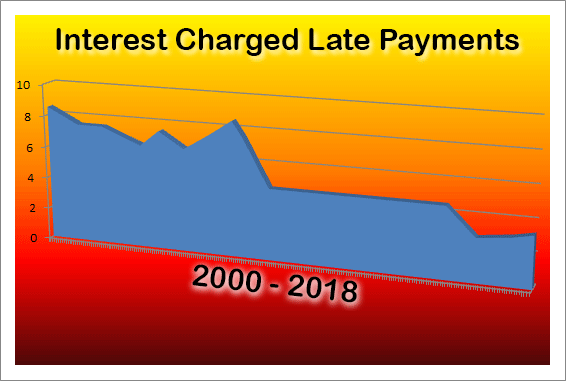

The interest HMRC charge for late payment varies each year, for example in 2007 it was a staggering 8.5%, in 2018 a slightly more palatable 3.25%

Penalties are subject to change; however this guide is correct at the time of writing. If you have missed any deadlines, get in contact with us straight away, the more time you give us, the better the outcome generally.

If I use an accountant, is the expense deductible?

By and large, as long as the accounting covers the business and nothing beyond the scope of your trade, the answer to this question is yes. For example, if you employ your accountant to complete a tax return online for your dog grooming company, its probably unacceptable to include your accountants fees where they also charged for bookkeeping your landscape gardening business.

This can be a little complex when setting up a business, and it warrants and article all to itself. We will link to this article when it is published, in the meantime, please contact us if you are unsure of accountancy fees and their status with HMRC.

How many people file their tax returns online

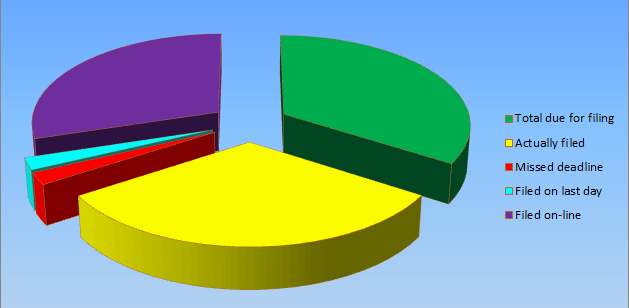

According to HMRC, in January 2019:

10,129,234 Self-Assessment tax returns were submitted online.

11,564,363 Self-Assessment tax returns were due.

10,833,177 Were received on time, or nearly 94%.

735,258 People left filing their tax return until the last day, with the majority of them filing between 16:00 – 17:00 on 31st January.

731,186 Missed the 31st January deadline completely.

What will I need to complete my self-assessment tax return online or by post?

As we continue with this article, hopefully with you completing your tax return alongside, I will try to expand on the type of things you need to include. For the moment, I am just going to go through the references and basic information you need to hand.

If you would like to complete a paper tax return, you can download it as a PDF (portable document format) file directly from HMRC. You can take a shortcut to https://www.gov.uk/government/publications/self-assessment-tax-return-sa100 and download the tax return year you would like to submit, the latest year being the first document on the page. If you would like to file your tax return online, you need to register for online services here https://www.gov.uk/log-in-register-hmrc-online-services/register . You can login using your government gateway to complete your tax return online here https://www.gov.uk/log-in-register-hmrc-online-services

Before you print the form, you will need to type the following information onto the PDF SA100 :

UTR – Unique Tax Payer Reference.

NINO – Also known as NI , your National Insurance ID.

Employer Reference – If you have one, if not leave it blank. If you are a sole trader, in self-employment only, this reference probably won’t apply.

Issue Address – Your address, the one you registered with HMRC.

Once you have that information added, go ahead and print the form, the rest is completed by hand.

Page TR1 – Starting your tax return.

This page completes the basic information about you. You should have completed your NINO if you are following this guide, and you won’t need to add it again into the area “National Insurance Number”.

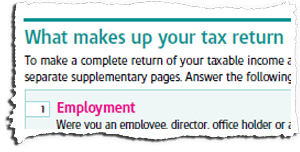

Page TR2 – What makes up your tax return.

The taxable income page asks you questions about your employment, that is, working for someone else, or a company. If you are a company director, you need to consider if you are employed. Is your company incorporated, for example as a limited company, registered with Companies House, or are you just using a trading style as a sole trader?

Most of the questions on this page require the downloading of additional pages to complete, known as supplementary pages. Some of these pages come in different varieties depending on your business size or needs; each has its own unique name, such as SA104F, and will need to be sent along with your tax return SA100. I plan to write articles to help you with each of these supplementary sheets, so do check the website for articles.

It is most likely you will answer “yes” to the next question about self-employment, as you are completing a self-assessment tax return. You may need to complete “self employment pages” for each business you operate, detailing expenses and payments for each one.

You can find SA103’s, which are short format self employment supplement pages at https://www.gov.uk/government/publications/self-assessment-self-employment-short-sa103s download the relevant year, and complete one for each business.

If your business is more complex, or are above the VAT threshold, you will need to complete the full format self-employment supplement pages at https://www.gov.uk/government/publications/self-assessment-self-employment-full-sa103f download the relevant year, and complete for each complex business.

The next question concerns partnerships, to be clear; we are talking about business partnerships, not a relationship partner! A business partnership is where two people or more take responsibility for the business, including any purchases you make, profit or losses. To add some complexity, it is possible for a limited company to be one of the business partners!

Similar to the self-employment supplemental pages, you can download short format partnership declaration form SA104S from https://www.gov.uk/government/publications/self-assessment-partnership-short-sa104s or full form SA104F from https://www.gov.uk/government/publications/self-assessment-partnership-full-sa104f .

UK Property is next on the tax return; do you receive income from any property you own or lease? This includes all kinds of property and land. If you have been following along, you can probably guess, there is of course a supplementary page for property details, you can download it here https://www.gov.uk/government/publications/self-assessment-uk-property-sa105 , it is known as an SA105.

The Foreign question applies if you have paid any tax abroad, have received any capital payment or benefit from any person abroad, or received or were entitled to any foreign income. If you think this applies to you, you can download the supplementary page here https://www.gov.uk/government/publications/self-assessment-foreign-sa106 , this page is referenced as a SA106.

The next question refers to trusts, that is to say, have you received or entitled to receive income from a trust, were settlor and put money or assets into a trust or settlement, or received income from a person who is deceased. This is quite a wide reaching question; even the supplementary form SA107 is named “Trusts etc”. You can download your trust return pages here https://www.gov.uk/government/publications/self-assessment-trusts-etc-sa107

The subject of capital gains can be a complex one, even HMRC themselves recommend you “ask your tax adviser” if you are in any doubt about this tax. If you have disposed of any assets including property, part shares in property, shares in a business, basically anything which has chargeable gains, you should include it in SA108, the supplemental pages for Capital Gains, which you can download from https://www.gov.uk/government/publications/self-assessment-capital-gains-summary-sa108

Residence, remittance basis may concern you if you have been living abroad in the tax year, have become a UK resident in the tax year, are not a resident in the UK, are domicile outside the UK, or even would like to use remittance basis for foreign income and/or capital gains. You can download form SA109 from https://www.gov.uk/government/publications/self-assessment-residence-remittance-basis-etc-sa109

Additional Information is a wide ranging question, and you should definitely download this supplement (SA101) to see what applies to you. Additional information includes things such as UK Securities, Life assurance policies, stock dividends, business receipts already taxed as income in a previous year, compensation and royalty payments, maintenance payments, married couples allowance, trade losses, tax avoidance schemes and disguised remuneration. Download SA101 here https://www.gov.uk/government/publications/self-assessment-additional-information-sa101

Finally for page TR2 you are asked if you need more supplementary pages, and if so, a link is provided, which is https://www.gov.uk/self-assessment-forms-and-helpsheets

If you complete your tax return online, the supplementary pages are automatically available for you to edit as part of your tax return.

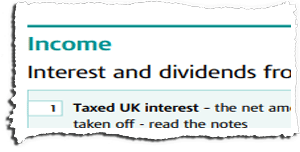

Page TR3 – Interest and dividends.

Page three of the self-assessment tax return covers money earned which is not necessarily part of your core business, and may have been earned with little or no effort on your part.

From your bank, building society, or savings in the UK, you will need to include what interest you have received. Firstly you need to indicate interest received where tax has already been deducted, and in the second area, interest received which has not already had tax taken off.

If you have any foreign accounts and have received untaxed interest or foreign dividends, and any tax deducted from those dividends.

You should also indicate here any domestic (UK) dividends you have received and any other dividends such as unit trusts or investment companies.

You should not include interest from ISA accounts.

If you are in receipt of a pension, you need to complete the details here, including state pensions and private. If you are receiving any state benefits such as incapacity benefit, jobseekers allowance, support allowance etc.

On page TR2 we have looked at several supplementary sheets you may need to complete, this last section of TR3 is for all the income you have received which can’t easily be classified to fit onto a supplementary sheet. An example might be payments received from a personal insurance policy to cover sickness or disability.

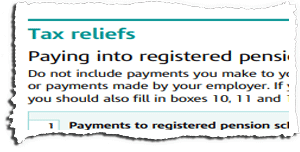

Page TR4 – Tax Reliefs.

Section TR4 includes tax relief for pension payments you have made, charity payments, and the blind person’s allowance.

You should check the documentation received from your pension provider, or contact them, to find out if you pension is classed as relief at source. This basically means tax relief is claimed by your pension provider. If you are younger than 75 years old, you can claim tax relief on pension payments providing you are UK resident, and had taxable UK earnings. You should not include your employers’ contributions to your pension here. The final part of this section, box 4, is for payments to overseas pension schemes that are eligible for tax relief.

Boxes 5 to 12 concern any charitable donations you have made within the tax year, it includes registered charities in the UK and abroad, not only monetary but also shares, land, property etc.

If you are registered blind or have severe sight difficulties and are registered as such with your local authority, questions 13 to 16 should be completed. If your partner has claimed the blind person’s allowance, but does not have enough taxable income to use all the allowance, cross box 15 if you wish to transfer the surplus to yourself. Conversely, if you are claiming the allowance, and would like your partner to benefit from any unused allowance, cross box 16.

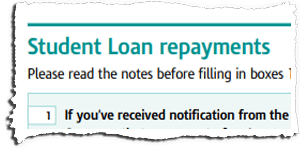

Page TR5 – Student Loans.

If you have been in receipt of a student loan, and you have received a letter from the Student Loan Company notifying payment has begun in the tax year, cross box 1.

If any payments have been deduced by an employer this tax year, add the payments into box 2. You will find your payments detailed on your P60 and/or PTA (Personal Tax Account).

Finally, if you think the loan will be paid-off within the next two years, cross box 3.

Child Benefit and High Income; If you earn over £50,000 and you or your partner receive child benefit, enter the amount of Child Benefit you and your partner received into box 1, the amount of children you received the benefit for, into box 2, and the date you stopped getting child benefit into box three.

If you are below the tax free allowance threshold and you are married, or are in a civil partnership, you can transfer your marriage allowance to your spouse or partner. To complete this section, you will need your partner/spouses civil national insurance number, their date of birth, and the date you were married/formed a civil partnership.

Page TR6 – Finishing your tax return.

If this is not an amended tax return, and you have received a tax rebate / refund, including repayments from the Job Centre, enter this amount into box 1.

Box 2 has two areas you can cross with an “X”. If you are due to pay less than £3,000 excluding class 2 national insurance contributions, HMRC can collect tax you owe directly from your wages or pension. If you do not want them to collect tax this way, you must cross the box. If you owe tax on savings, property income, child benefit payments etc, and would like HMRC to collect any due tax, leave this box blank.

Boxes 4 to 14 need completion if you are expecting a tax rebate or refund from the details you have given in this self-assessment tax return. You will need your bank account or building society account details before completing this section, and details of your accountant / tax adviser if you choose to use one. Remember to sign this section for repayment to go to your indicated nominee.

Page TR7 – Your tax adviser.

If you are using a tax adviser, you can complete their details in boxes 15-18. This is entirely optional, however if you have included them as a nominee in the previous section, it may be helpful to include their details here.

Box 19 gives the opportunity for you to include any further information which could not be included elsewhere on the tax return. For example, you may have included information about foreign pension payments; this box would be a good place to include extra details of the pension company.

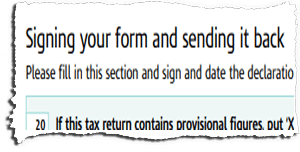

Page TR8 – Signing your tax return.

The final page of your tax return should be fairly straightforward, at least, once the first two questions are answered.

Box 20 , if you have included provisional figures in your tax return, put an X in the box. If you have supplied provisional figures, you should use Box 19 on Page TR7 to explain why, and when you will be expecting to supply accurate figures.

Box 21, if you have completed supplementary documents such as SA103, SA104, SA105 etc. mark X in this box.

Box 22 simply requires your signature and todays date.

Boxes 23 to 26 need only be completed if you are acting on behalf of someone else, such as:

- You are the executor in a deceased persons will.

- You have power of attorney for someone who needs

to complete a tax return, but isn’t capable. - You have been appointed by a UK court to

complete the return for someone else.

Tax Return – Final thoughts

If you are completing a paper tax return, it might not be clear how much tax you have to pay, however as long as you get your tax return to HMRC by the October 31st deadline, they will write to you letting you know how much tax you need to pay (if any). You will then have up until the following January 31st to make the payment to HMRC.

Completing your tax return online should give you an indication of the tax you will need to pay straight away. Employing the services of a professional accountancy firm will allow you to know what tax you will be required to pay, before your tax return is submitted to HMRC.

I hope you found this guide useful, however it cannot take the place of professional advice given from your accountant, and we do not take responsibility for any errors in this document, and do be aware, things may have changed since this document was written. While I have concentrated here on the postal returns, the questions for the tax return online system are the same, and should translate easily for you. If you have any questions or need help with your tax return, please contact us.